This paper was co-authored by Lily Dai, Senior Research Lead, Sustainable Investment Research, FTSE Russell; Jaakko Kooroshy, Global Head of Sustainable Investment Research, FTSE Russell; Rachel Teo, Head of Sustainability and Total Portfolio Sustainable Investing, GIC; Wong De Rui, Lead, Sustainable Investment Research, Sustainability Office, GIC; Deborah Ng, Head of ESG and Sustainability, GMO; Christopher Heelan, Quantitative Research Analyst, ESG Research Platform, GMO; Kenneth Hsu, Quantitative Research Analyst, ESG Research Platform, GMO; and Timothy J. Wheeler, Quantitative Research Analyst, ESG Research Platform, GMO.

The authors would like to thank Ng Xiang Long, Trang Chu Minh and Nicholas Goh (GIC), David King and George Sakoulis (GMO), Alberto Allegrucci and Lee Clements (FTSE Russell) for providing valuable comments and suggestions. The report, however, reflects the methodological choice and views of the authors alone.

Transitioning to a green net-zero economy requires climate solutions that enable the economy to decarbonise, such as renewable energy, electric vehicles, and recycling technologies. This also creates significant investment opportunities – companies providing climate and environmental solutions have been growing and outperforming the market over the last decade. The economics of climate solutions are making fossil-fuel-dependent assets less attractive from a financial point of view. These companies are likely to grow even more as economies progress on their net-zero goals.

There is an emerging toolbox for systematically identifying and managing portfolio exposure to climate-related investment opportunities. Different metrics are typically employed across investors and asset classes, such as dollar amount invested in green bonds for fixed income and renewable energy generation for infrastructure. These metrics, while helpful for measuring specific sectors or asset classes, are challenging for investors to use due to their lack of comparability.

To address challenges in measuring climate solutions exposure, this paper examines four metrics: green revenue, green capex, green patents and avoided emissions that are broadly applicable in a portfolio management context. Each metric has its pros and cons but, altogether, they provide a comprehensive view of the available metrics to assess companies’ exposure to climate solutions. This paper focuses on green revenue based on its benefits. Green revenue is easier to interpret, directly links to companies’ cash flows and real-world impact, and the data is more readily available and comparable.

We find Weighted Average Green Revenue (WAGR) to be the most promising metric currently for integrating climate solutions measurements into portfolio construction. It builds on the portfolio weighting methodology used in carbon metrics such as Weighted Average Carbon Intensity (WACI) that is widely adopted by investors. WAGR calculates the green revenue percentage (GR%) of a portfolio by applying company GR% to the portfolio weight of each company. Investors can set portfolio-level targets of climate solutions using WAGR, such as a minimum level, an improvement relative to the benchmark, or to track specific WAGR pathways such as decarbonisation trajectories.

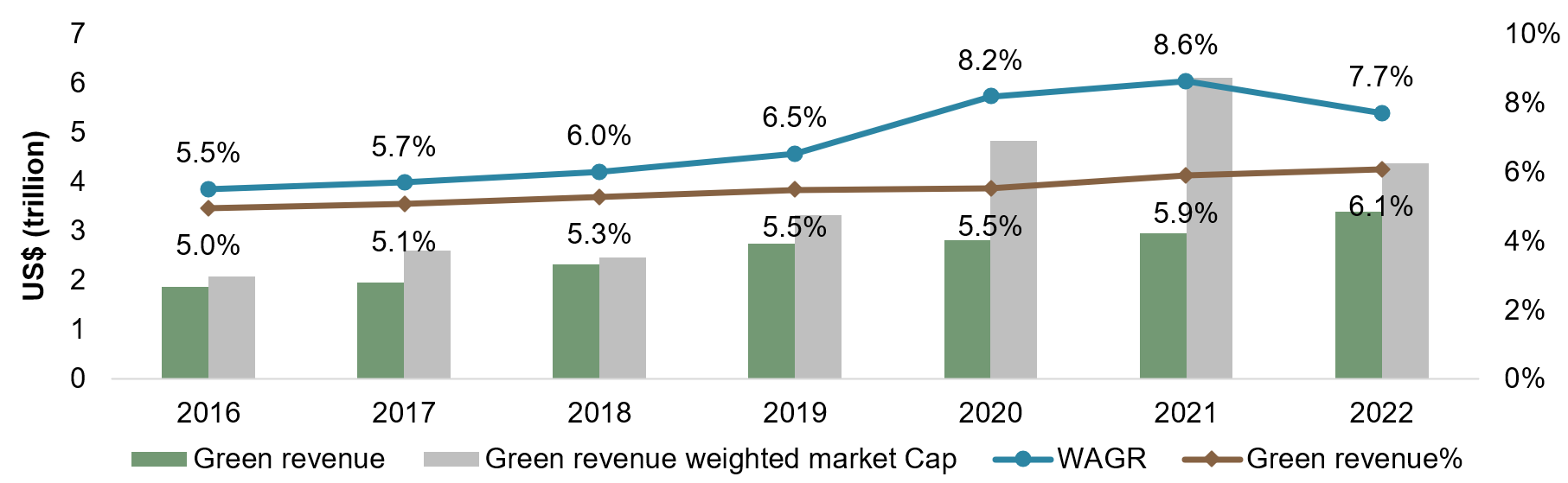

Using WAGR, this paper analyses portfolio exposure to climate solutions, including size, growth, industries, green sectors, regions, and the level of ‘greenness’ (shown by the tiering structure under the FTSE Russell Green Revenues Classification System), with the FTSE All-World Index as the reference portfolio. Figure 1 shows that FTSE All-World’s WAGR grew from 5.5% to 8.6% between 2016 and 2021 and fell during the down market of 2022. In comparison, FTSE All-World’s unweighted green revenues record a steadier year-on-year growth, which reflects the ‘value impact’ of market capitalisation.

Figure 1: WAGR of the FTSE All-World

Source: FTSE Russell, April 2023.

Akin to WACI, potential investor applications of WAGR include climate reporting against frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD), target setting, thematic investing and corporate engagement. Investors should acknowledge the constraints and trade-offs when building portfolios with a significantly greater WAGR, such as sector and country concentration, volatility and the size of the universe.

Disclosures based on green revenues are still nascent and would likely improve over time with the adoption of reporting based on different green taxonomies. In addition, climate-related disclosures in private markets, including green revenue data, continue to be in short supply, which limits access to comparable data across different asset classes for investors. This paper aims to raise greater awareness of the value of WAGR to assess and integrate green opportunities into portfolio construction, which in turn will encourage greater disclosures. In conjunction with other sustainability metrics, WAGR can be a useful tool to calibrate and measure exposure to climate solutions in a portfolio management context.

Please click on “Save As PDF” for the full paper.