At GIC, we expect a difficult investment environment with modest growth prospects, greater uncertainty and a high degree of volatility in the macro economy and markets. The long-term (20-year) returns in the coming years are likely to be significantly lower than what we saw since 1980.

Looking back: High returns from the mid-80s were an exceptional phase in investment markets

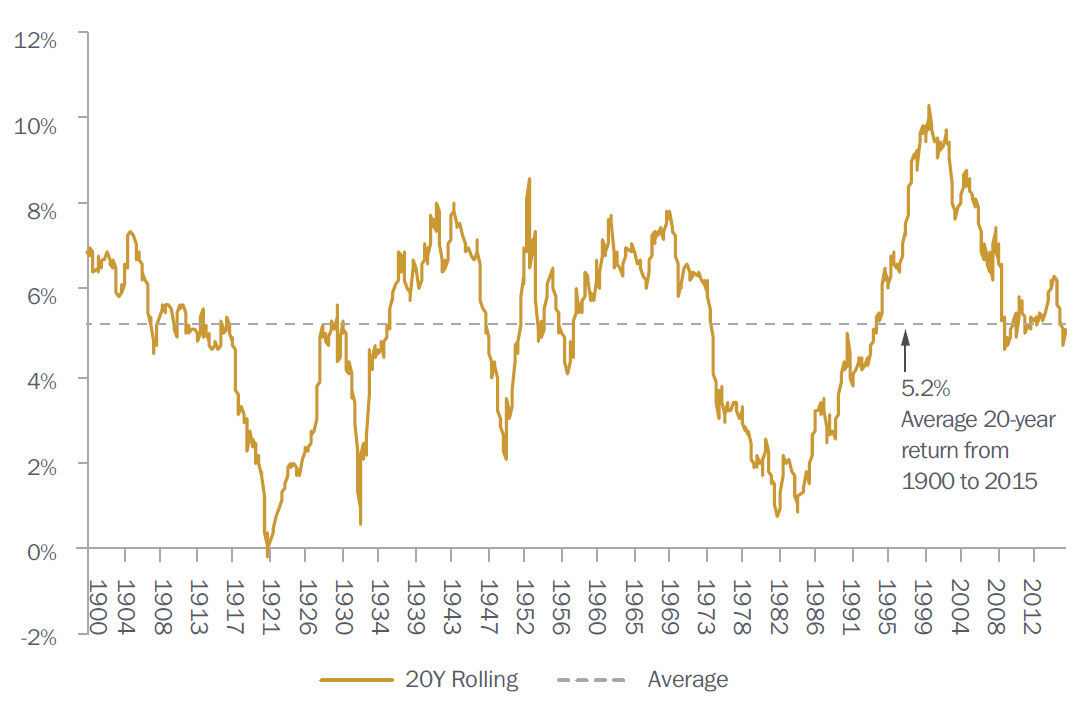

Long-term returns can vary substantially over time, even when averaged over 20 years. Looking at a US portfolio of 65% stocks and 35% bonds (for which long-term historical data is available), the annualised 20-year rolling real return has varied very widely around the 5.2% average generated between 1900 and 2015 (see Figure 1). For example, the 20-year real return was below 2% for much of the first half of the 1980s, and was as high as 10% in 2000.

Figure 1: 20-Year rolling real return of a US 65% stocks/35% bonds portfolio from 1900 to 2015

The 20 years ending 2000 which saw outsized returns were in fact an exceptional period in investment history. The strong performance of assets during this period was driven by low starting valuations and the subsequent substantial, fundamental improvements in the world economy. In the early 1980s, nominal bond yields and equity earnings yields in the US were at historical highs, reflecting the US Fed’s battle against inflation. Assets were hence priced low as investors discounted futures earnings with higher interest rates; while earnings expectations were also modest, shaped by the earlier period of poor economic performance. As it turned out, interest rates fell sharply in the years that followed, and the subsequent economic performance was significantly more positive than expected.

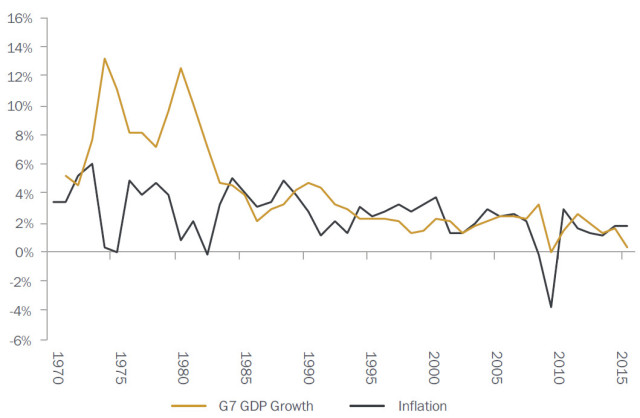

The more positive economic outcome could be explained by three factors. First, structural economic changes and improved policies, especially monetary policy, curbed macroeconomic volatility, lowered inflation and drove down interest rates in many advanced economies (see Figure 2, below). In the US, for example, the inflation rate fell from about 10% in 1981 to around 2% by 1986 after a sharp tightening of monetary policy and a deep recession, and has stayed benign since then. During the 20-year period, 10-year US nominal interest rates fell dramatically from 14% in 1981 to 6% in 2000, causing capital gains in many asset classes. Second, trade liberalisation and growth-enhancing reforms in emerging markets further boosted global growth and trade. The entry of China and former Soviet Bloc countries into the world economy added to these disinflationary forces. Third, the information technology revolution raised global productivity. In financial markets, the productivity improvement fed overly optimistic expectations in the late 1990s, and temporarily boosted paper gains on technology stocks.

Figure 2: Lower volatility in growth & inflation from mid-1980s

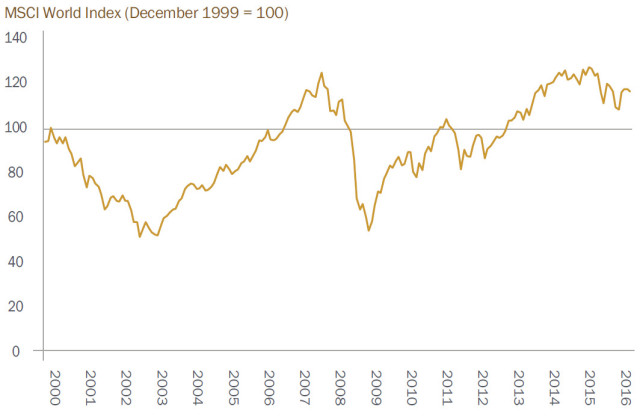

Figure 3: Gyrations in the MSCI World Stock Market Index since 2000

Since 2000, asset returns have experienced a number of large moves, including the crash of the Tech Bubble (2001), the US Credit/Housing Bubble (2003-2007), the Great Financial Crisis and the European Economic and Monetary Union Crisis (2008-2011), and the strong policy-induced recovery (2010-2015). Figure 3 shows the gyrations in the MSCI World Stock Market Index. As a result of the volatile boom-bust investment environment, especially for the stock market since 2000, by the end of 2015 the annualised 20-year rolling real return of the US 65/35 portfolio had fallen to 5.1% (refer to Figure 1, above).

Low expected returns over the next 10 to 20 years

We expect low returns from markets over the next 10 to 20 years, due to three factors. First, current valuations of assets are high, and as earlier mentioned, starting asset valuations are a good indicator of future returns. Second, the prevailing historically low interest rates are likely to rise over time, removing an important support for the currently high valuation of assets. Third, the fundamental outlook for future growth and earnings is a modest one with great uncertainty. This will weigh on the prospects of asset returns.

High starting valuations

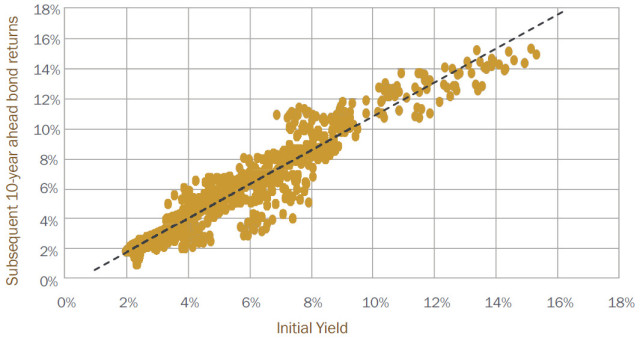

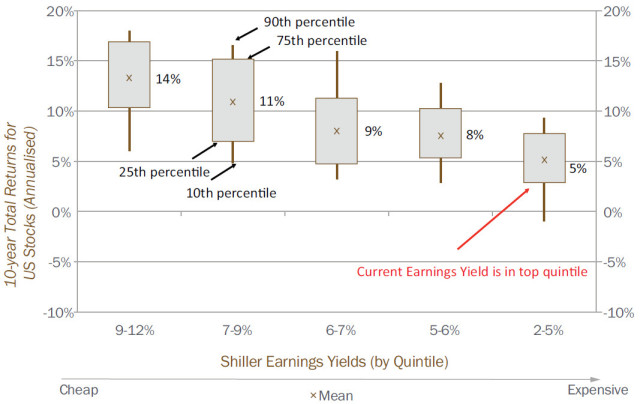

Medium- to long-term future asset returns are determined by starting valuations and the subsequent fundamental performance. Starting valuations (as proxied by asset yields) are a particularly useful indicator given that they are known today. For bonds, the correlation between beginning yield and final returns is almost 1 (see Figure 4, below). For equities, a fairly good indicator of future returns is the current Shiller earnings yield. This is defined as the average of 10 years of earnings, adjusted for inflation, divided by the share price of a company or index. It can be used to assess the likely future returns from equities over the medium- to long-term. Figure 5 (below) shows the correlation between the nominal Shiller earnings yield and future equity returns.

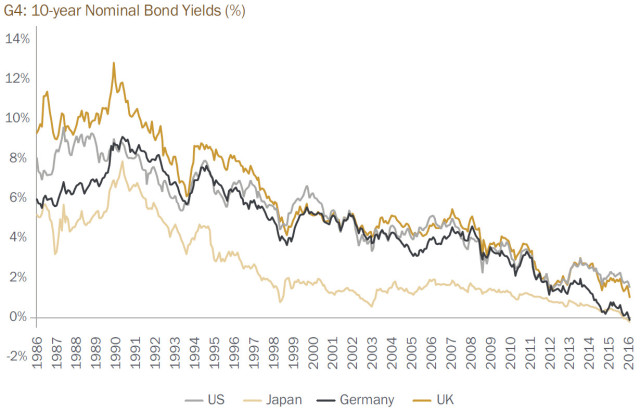

Historically low interest rates expected to rise over time

Interest rates are unlikely to go much lower than their current low levels (see Figure 6, below). As at end June 2016, about 30% of global bond markets, or approximately US$13 trillion of bonds, were offered with negative nominal yields. This means investors must in effect pay interest to invest in these fixed income instruments rather than receive interest for doing so.

In the short to medium term, we expect interest rates to stay at current levels, or rise modestly due to the weak economic outlook. However, even small increases in interest rates will weigh on asset prices and reduce potential returns. Interest rates, as an important component of the discount rate of future cash flows, significantly affect the equity value of companies. Higher interest rates will raise discount rates, and lower the present values of assets.

Figure 4: 10-year US bond returns vs initial yields (1900 – 2016)

Figure 5: Future equity returns given Shiller Earnings Yield (1900 – present)

Figure 6: Historically low interest rates

Modest and uncertain growth fundamentals

Besides high starting valuations, the fundamental outlook for assets is also subdued and uncertain. We anticipate three possible scenarios for the next 10 to 20 years. One scenario is that of a “back to normal” world, where over time the global economy and financial markets recover. Growth in the developed world turns out somewhat lower but this is offset by China and India, although all the major countries will be dealing with aging populations. In this scenario, interest rates will rise, though slowly, while equities will benefit from continued growth. We expect that over 20 years, taking into account both starting valuations and the fundamentals in this “back to normal world”, real annualised returns on global bonds would be 0-1% and that of global equities around 3%.

In the second scenario, the global economy is in “stagnation” for a long period of time. This may be triggered by a US recession, the Eurozone breaking up, or a China hard-landing. Regardless the cause, it will be much more difficult for central banks to maintain confidence. Political and social forces will also push for de-globalisation, resulting in trade and investment restrictions. These combined factors will trap the global economy in sub-par, mediocre growth for a long period of time. In such a world, we would expect bonds to perform better while equities suffer.

The third and last scenario is “stagflation”. This occurs because a combination of high debt, easy monetary policy, and populism eventually results in many countries tolerating higher inflation. Economic growth, however, does not improve. In this scenario, both bonds and equities would perform poorly.

How GIC invests in a low-yield, high uncertainty environment

GIC anticipates significantly lower and more volatile returns in the next 10 to 20 years, compared to our experience in the last two to three decades. Our key sources of return will remain the Policy Portfolio and the Active Portfolio. While our investment framework and approach remain sound, we will need to adjust some parts of our strategy as conditions change. We will continue to emphasise generating returns through a long-term, diversified and relatively conservative portfolio.

Policy Portfolio

Most critically, we have to ensure that our portfolio does reasonably well in a range of plausible scenarios. This means the portfolio needs to be diversified along multiple dimensions (such as across different regions and return drivers), keep its overall risk within our tolerance threshold, and have a mix that allows us to harvest risk premiums over the long term. We will also continue to explore new asset classes and portfolio construction approaches.

Active Portfolio

For a number of years, GIC has focused on building a diversified portfolio of active investment strategies. Our investment framework guides us in allocating risk capital to strategies that are expected to add to overall portfolio returns. In the new environment we will continue to do so, and be even more vigilant as both risks and opportunities are likely to increase. In addition, we will strive harder to reduce portfolio costs as any such savings are direct additions to our portfolio returns.

Conclusion

Looking ahead, we expect a difficult investment environment with modest growth prospects, greater uncertainty and more volatility in the macro economy and markets. The long-term (20-year) returns are likely to be significantly lower than what we saw since 1980. Nonetheless, our investment philosophy, governance framework, organizational capabilities and market network, all carefully developed since 1981, leave us well-placed to invest in this new environment.