This paper was co-authored by Wong De Rui, Lead, Sustainable Investment Research, Sustainability Office, and Rachel Teo, Head of Sustainability and Total Portfolio Sustainable Investing at GIC.

Introduction

Climate issues are complex, multi-faceted and fast-evolving. GIC has established that climate change affects asset returns through three channels: physical risks, transition risks and, market risks. Significant uncertainty surrounds these risk drivers, and climate scenario analysis helps us understand their possible pathways. We used a combination of approaches, both top-down and bottom-up, to examine the range of impacts on investment portfolios and to identify critical pockets of risk.

Alongside climate scenario analysis, forming a view on the relative likelihoods of the climate scenarios is important for nimbly managing our investment portfolio and bolstering its resilience across different future plausible states of the world. This task, however, is complicated by dissenting views among experts in different domains.

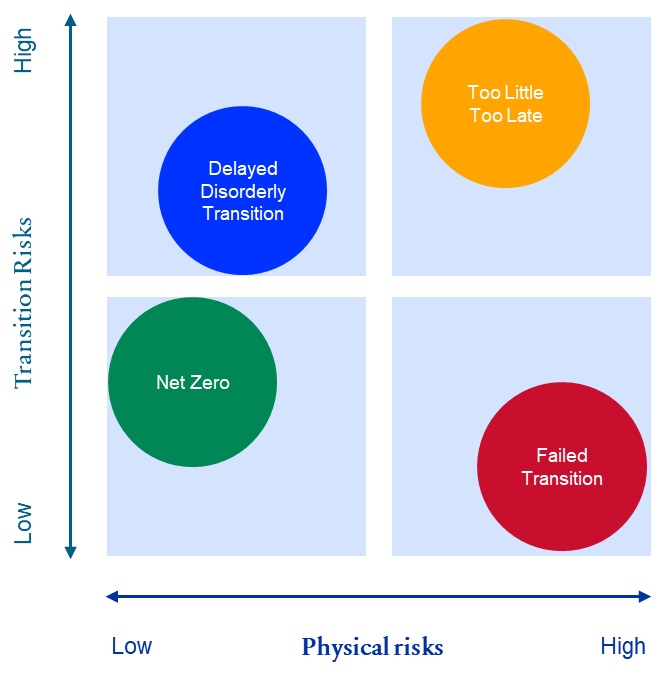

To reconcile competing expert opinions, various investment organisations have developed tools to track the progress of the climate transition and navigate uncertainties surrounding it. At GIC, we have developed the GIC Climate Signposts (GCS) to provide a holistic and balanced appraisal of the likelihood of GIC’s four main climate scenarios: Net Zero (NZ), Delayed Disorderly Transition (DDT), Too Little Too Late (TLTL), and Failed Transition (FT). Figure 1 illustrates where these climate scenarios reside on the spectra of physical risks and transition risks.

Figure 1: Physical vs transition risk impacts in GIC’s climate scenario set

Source: GIC, Ortec Finance

The GCS uses a range of indicators covering four dimensions: countries, businesses, technology, and the physical environment. They include indicators of the future and present, of words and deeds, and across key stakeholders and drivers of decarbonisation. Figure 2 provides an overview of the indicators used in the climate signposts. See Appendix A for more details on the methodology.

Figure 2: Overview of the GIC Climate Signpost indicators across four dimensions

Source: GIC

Findings

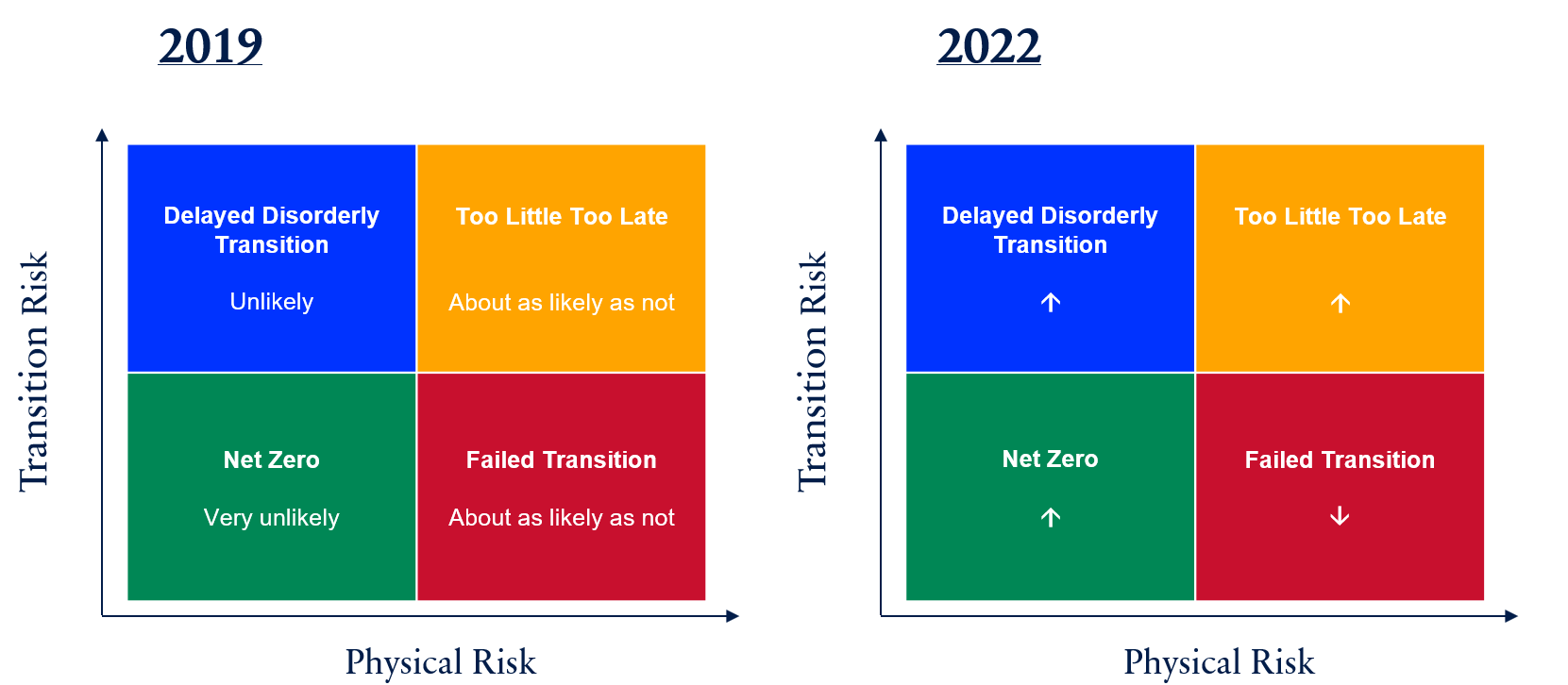

The present scenario probabilities in descending order are: Too Little Too Late, Failed Transition, Delayed Disorderly Transition, and Net Zero.

The GCS indicates progress towards a successful transition, defined as keeping global warming below 2⁰C by 2100, being made over the last three years. The best (Net Zero) and worst (Failed Transition) outcome improved and declined in likelihood, respectively. (See Figure 3). This is because of a rise in net-zero pledges by governments and businesses, improved public awareness of the urgency of climate action and increased investments in the solutions required to accelerate the green transition.

Figure 3: Climate scenario probabilities in 2019 vs 2022

*Arrows in 2022 denote an increase or decrease in probabilities.

Source: GIC calculations based on data from BloombergNEF, Cambridge Econometrics, Climate Action Tracker, the Climate Change Performance Index Report, the Global CSS Institute, Google Trends, the IEA, McKinsey, MSCI, NGFS, Ortec Finance, S&P Trucost, etc.

Three key insights from the GCS and their investor implications:

- High degree of climate scenario uncertainty: No climate scenario has more than 50% probability. However, none can be completely ruled out either. Investors who optimise their portfolio for a single scenario risk getting blindsided.

- Elevated transition and physical risks: Scenarios with high physical risks are “Likely” and those with high transition risks are “As Likely As Not”. Investors cannot only focus on managing transition risks – addressing physical risks is equally important.

- Climate progress disguises disruptive change on the horizon: The fall in probability of the worst-case scenario, a Failed Transition, over the last three years is driven in part by strengthening country commitments, which can be a leading indicator of future action.

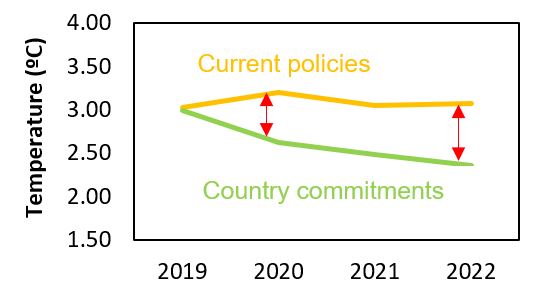

There is a widening gap between countries’ words and deeds as countries appear to accelerate their commitments even as actual policymaking lags behind (Figure 4). Any rapid closing of the widening gap could precipitate disruptive change. Investors must prepare to navigate heightened volatility when stronger climate actions materialise.

Figure 4: Gap between current policies and commitments of countries

Source: GIC calculations based on data from Climate Action Tracker and the Climate Change Performance Index Report.

Conclusion

The GCS enables GIC and our peers to think beyond binary outcomes of whether the world is on track to meet the climate goals set by the Paris Agreement, by allowing a more nuanced probability assessment. This provides a useful reference point as we work towards strengthening the integration of climate risks in our portfolios, whether through more in-depth due diligence on physical risks or by accounting for transition risks through carbon price stress tests and/or climate value-at-risk analyses.

The GCS probabilities provide an outlook based on the state of the world today. Too Little Too Late is the marginally predominant scenario at this time, although encouragingly the Failed Transition probability has declined considerably thanks to country and industry commitments and policies. We anticipate further changes ahead, although the future is uncertain. Given the non-zero probabilities of all four climate scenarios and the fact that they will continue to change, investors should manage their portfolios nimbly and optimise for a range of climate outcomes.

Importantly, climate risk integration must be carried out at both the top-down and bottom-up levels to gain a holistic and nuanced view of a portfolio’s climate risks and investee companies’ climate resilience plans. Bottom-up strategies must also prepare for the economic volatility that might result from a potential disruptive transition that is increasingly more likely to unfold.

As with other climate-related analytics, the GCS is an evolving tool, and we welcome feedback from the investment community on improving it.

Please click on “Save As PDF” for the full paper.