This article was written by Rachel Teo, Head of the Futures Unit and Senior Vice President, and Wong De Rui, Vice President, Economics & Investment Strategy, GIC.

Introduction

Economic inequality matters for investors as it affects the macro investment environment that we operate in. This is especially pertinent now, with several recent IMF studies showing that inequality is expected to increase discernibly after the pandemic. Left unmitigated, economic inequality poses disruptive threats to the economy, society, political stability, and ultimately financial markets and investments. Moreover, research done by GIC’s Futures Unit found that economic inequality hurts growth and exacerbates inflation; is correlated with higher political instability, and breeds populism that undermines multilateralism and democratic institutions. All these lead to increased economic and investment risks over the long term.

To explain this relationship further, GIC created a Composite Inequality Index (CII) that captured three dimensions of economic inequality – income, wealth and opportunities (encompassing unequal access based on socio-economic backgrounds or gender). The results, as outlined in this paper, show that broad inequality indeed correlates with weaker economies, populism and less stable politics, and higher risk premiums, indicating greater risk to long-term equity returns. Inequality is a material long-term investment issue, as more investors recognise its implications on the financial performance of their assets over time.

“Broad inequality indeed correlates with weaker economies, populism and less stable politics, and higher risk premiums, indicating greater risk to long-term equity returns.”

Inequality – finding a better measure

The measure of inequality is typically associated with the Gini coefficient, which focuses on income (and sometimes wealth). While useful, it is an incomplete measure, with economic inequality increasingly recognised as an issue involving not just income and wealth, but opportunity as well. Seeing the need to define and measure economic inequality more accurately, the GIC Futures Unit developed the Composite Inequality Index based on both Opportunities (and access to opportunities) and Outcomes (the more traditional measures of income and wealth).

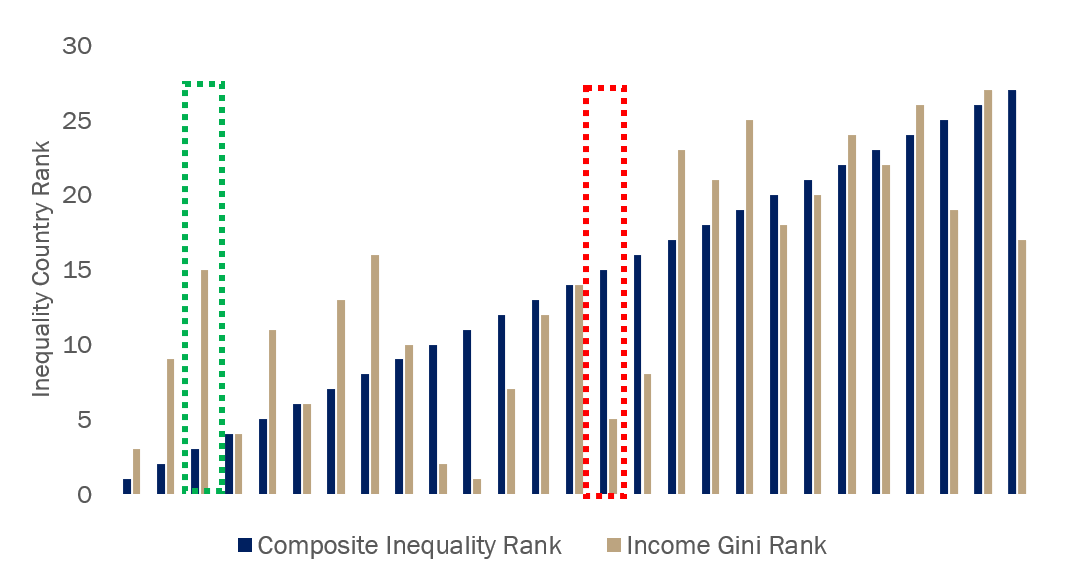

Exhibit 1 shows the inequality ranking of 27 countries based on our CII framework and compares this with the Gini coefficient. The CII shows a different inequality picture from only focusing on the income Gini coefficient.

Exhibit 1. Comparison of Country’s Rank based on the CII vs the Gini Coefficient

Note: A higher number denotes greater inequality. Source: GIC calculations

For example, a middling performer on the income Gini coefficient can be one of the best performers on the CII (example highlighted in the green box). This is because the country’s average performance in income inequality is more than offset by strongly positive showings in wealth distribution and access to opportunities, particularly in the areas of intergenerational mobility and gender pay gaps.

Conversely, a country that scores well on the income Gini coefficient can be average on the CII (example highlighted in the red box). This country’s performance in opportunities is average and the difference is largely due to the severe wealth inequality offsetting its relatively more equal income distribution. Factors driving the wealth inequality include negligible wealth taxes and favourable homeownership tax policies (e.g. tax rebates on mortgage interest payments and tax deductions for maintenance, refurbishments and household services) that enable homeowners to accumulate wealth faster.

In the subsequent section, we argue that investors must worry about economic inequality because of its impact on the macroeconomic environment, politics, policies, and markets. Many studies have established the relationship between economic inequality and macroeconomic variables such as growth and inflation, while the implications of economic inequality on the political environment, policy landscape and drivers of market returns are not as well researched. We employed our CII to examine how economic inequality affected political stability, the rise of populism, country risk premiums and equity market returns. We summarise our findings below.

Impact of inequality on growth and inflation

A wide range of past research concluded that inequality hurts economic growth especially in middle- and high-income countries and exacerbates inflation.

Growth

Inequality reduces GDP growth by impeding labour productivity and consumption growth. Rising economic inequality could result in poorer human capital quality due to limited access to credit, education and healthcare. Labour productivity is also potentially lower if significant parts of the population face challenges with employment, or are unable to acquire the new skills needed for and share in the benefits of technological innovation. Consumption is undermined by prolonged weak or stagnant income growth for lower income groups, especially because these groups also typically have a higher propensity to consume out of income.

According to studies by the IMF and OECD, a 1 percentage point (ppt) deterioration (increase) in the income Gini ratio was associated with 0.07 to 0.12 ppt reduction in annual GDP growth. Using our CII, a 1 ppt increase in broad inequality shrinks a national economy’s GDP by 0.12 ppt.

Inflation

Inequality worsens inflation as a result of arguably less equitable policies. Societies with higher inequality tend to see higher income groups preferring inflation to taxation when it comes to financing government spending, given the more progressive nature of income and wealth-related taxes. There is also a preference for monetary easing to support asset prices when economic conditions turn unfavourable, which leads to higher inflation in the longer term.

Other studies found that an increase in the Gini coefficient of 1 ppt was associated with 0.4 to 1.3 ppt increase in inflation. Our CII saw a similar relationship, with a 1 ppt increase in broad inequality corresponding with a 0.8 ppt increase in inflation.

Impact of inequality on political stability and populism

Our research showed that economic inequality has a negative impact on political stability and is one of the key drivers of populism. We saw this in the deterioration of political stability and rise in populism across both Emerging Markets (EM) and Developed Markets (DM) in recent years.

Political Stability

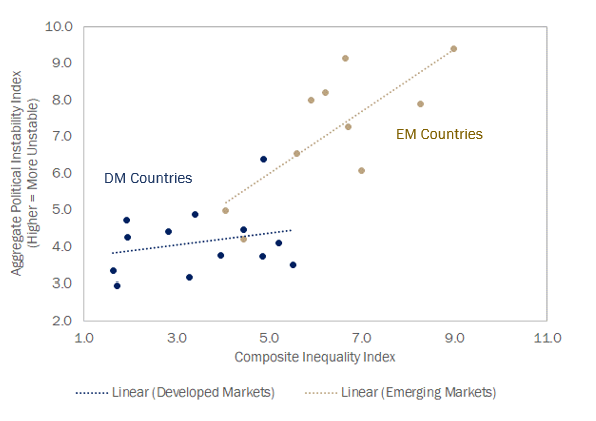

As shown in Exhibit 2, based on an aggregate index of six indicators of political instability, there is a robust positive relationship between inequality and political instability across EMs and DMs.

Exhibit 2: Inequality and Political Instability

Source: Fund for Peace, Vision of Humanity, Transparency International, World Bank, PRS Group, GIC calculations.

Populism

Populism is difficult to define and quantify. To facilitate analysis, we defined a country’s receptivity to populism as the vote share garnered by its populist parties. Populist parties were in turn identified by political rhetoric emphasising (i) direct representation of the people and (ii) the failings of the current establishment. We found this to be a useful working definition that is increasingly gaining consensus in the research community as well.

Populist parties and politicians tend to emerge in countries with higher levels of inequality, financial globalisation and corruption perception. This is because gains from financial globalisation and corruption largely accrue to the rich and well connected, accentuate inequality and reinforce the average voter’s feelings of unfairness and exclusion.

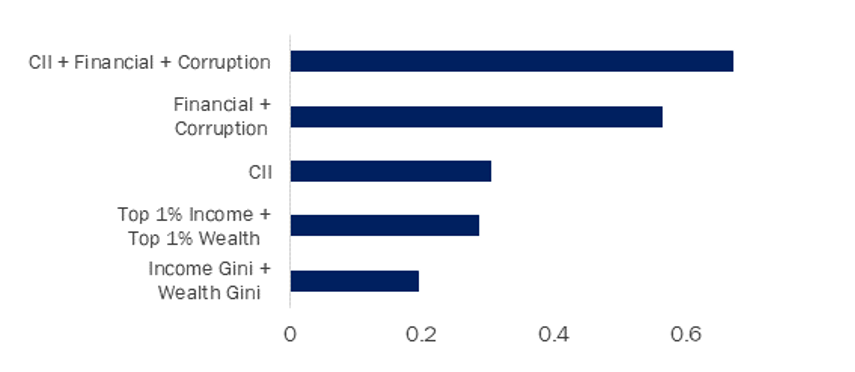

The combination of the CII, together with measures of financial globalisation and corruption perception, explained the rise of populism well (with a high r-squared of 0.7). As seen in Exhibit 3, the CII explained rising populism better than other measures of inequality such as income and wealth Gini coefficients.

Exhibit 3: Adjusted R2 of Select Drivers Mix Against Country’s Populism

Source: GIC calculations.

We conducted further analysis to understand the implications of rising populism on the policy environment. Did populist parties address and reverse underlying inequality issues and improve the stability of societies? Unfortunately, our research showed that populist parties’ policies hardly addressed the redistribution concerns of the very electorate that voted them into power, and instead risked exacerbating inequality. Populist parties are more likely to implement policies that undermine multilateralism (e.g. higher import tariffs, reject participation in international organizations or regional collaborations) and democratic institutions (e.g. weakening existing checks and balances on executive power and diminishing central bank independence). These policies detract from economic growth and stability, and correspondingly, increase the riskiness of investing in these countries.

History also showed that inequality was often only reversed through transformative revolutions, mass mobilisation wars, state collapses or catastrophic pandemics. There is thus an urgent need to address inequality through more benign means, such as improving access to education, healthcare, credit for the low-income/wealth groups, and ensuring they have access to good employment opportunities.

Impact of inequality on drivers of financial returns

The implications of inequality on financial returns are limited and less clear-cut in academic literature. Using our CII, we identified an intuitive result for risk premiums, but a potentially unintuitive one for equity returns.

Country Risk Premiums

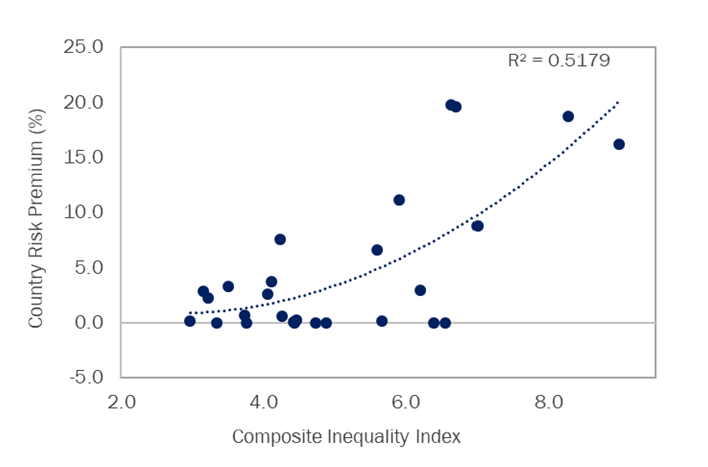

Countries with greater inequality tend to have higher country risk premiums and the relationship is non-linear (Exhibit 4). Country risk premiums surged when inequality crossed a certain threshold. The reasons for this are the harmful relationships between inequality and economic growth, inflation and political stability described earlier. Given this, investors would thus demand a higher risk premium to invest in countries that are more unequal.

Exhibit 4: Inequality and Country Risk Premium

Source: Refinitiv, GIC calculations.

Inequality and Equity Returns

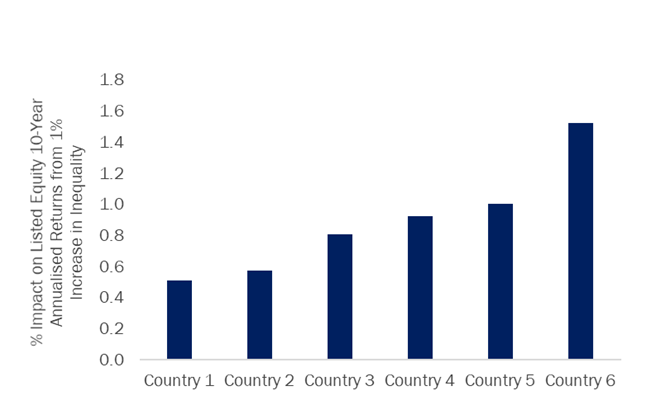

The links between inequality and equity returns are more complex, and our analysis found a positive relationship between inequality and listed equity returns for major countries in DM and EM (see Exhibit 5). This reflected the wealth accumulation process for the higher income groups. Controlling for variables such as GDP growth, inflation, policy rates and wages, a 1% increase in inequality increased 10-year annualised equity returns by 0.5% to 1.5% in these countries.

Exhibit 5: Impact of 1% Increase in Inequality on Listed Equity Returns in Selected DM and EM Countries

Source: GIC calculations.

This result appeared to run counter to the findings that inequality had a negative impact on economic growth (and one could assume, investment returns), but it reflected the wealth accumulation process in the economy. We explored this from the perspective of Valuations and EPS (Earnings Per Share) Growth.

Valuations: When capital in the economy is increasingly concentrated in the hands of the wealthy, who have a higher propensity to save and invest than the poor, more funds are channeled into risky assets that drive up valuations.

EPS Growth: Profit margins benefit from a declining wage share as companies are in a stronger bargaining power relative to workers. This is due to (i) pro-business policies like deregulation and the weakening of labour unions (ii) globalisation which allows firms to source for the lowest cost labour (after adjusting for productivity) and (iii) technology as a key driver of value creation in the last 20 years which not only reduced aggregate demand for labour but favoured a smaller group of highly-skilled workers over the average employee. The political channel also cannot be ignored. Large companies with more resources and influence would lobby for more favourable business policies that inadvertently worsen economic inequality.

There is also corporate inequality, which is a function of larger and more dominant firms having better access to capital, technology/R&D resources, which raises barriers to entry and drive relative outperformance.

Hence, we see this positive relationship historically observed between inequality and equity returns to be contingent on pro-business policies and weak wage growth remaining intact to support profitability. However, inequality is either high or has worsened considerably in many countries. This calls into question whether it would cause the rise of populism and changes in the policy environment that had benefitted owners of the equity markets. For example, we are seeing more pressures on politicians and policymakers to protect domestic industries, goods and services against foreign competition. In addition, in the longer term, there is the risk that weak top-line growth, especially for the average firm, could more than offset the declining wage share benefit that companies had previously enjoyed.

Practical takeaways for investors

COVID-19 has highlighted the vulnerabilities of rising inequality, specifically those with limited or no access to vaccines, healthcare, jobs, social safety nets, and technology. This economic and social divide will only widen further, given the continued digitalisation shift and increased automation. Research by GIC’s Futures Unit has highlighted the impact of inequality trends on the macro environment, and the potential risks to investment returns over the longer term. We outline two ways for investors to factor inequality into their top-down and bottom-up investment processes.

First, long-term expected returns may change significantly. In terms of asset allocation, we need to think about how inequality trends could affect the different countries we invest in. For instance, investors may need to adjust their assumptions about growth, inflation and country risk premiums, and look at how to incorporate inequality-related risk scenarios like stagflation or populism into asset allocation research.

Second, inequality needs to be addressed one way or another. There are opportunities for investors to do well and do good by investing in commercial solutions that mitigate income/wealth inequality. These include companies that increase education, healthcare, and credit access for the lower income groups.

“Inequality needs to be addressed one way or another. There are opportunities for investors to do well and do good by investing in commercial solutions that mitigate income/wealth inequality. These include companies that increase education, healthcare, and credit access for the lower income groups.”

Inequality could be a material long-term investment issue as more investors recognise its implications on the financial performance of their assets. We hope this piece contributes to the conversation in preparing investment portfolios for the ramifications of inequality.