This article was adapted from a fireside chat between GIC CEO Lim Chow Kiat, and Uday Kotak, Founder, Managing Director and CEO of Kotak Mahindra Bank Limited, during the CII Conference in December 2021. Their discussion focused on GIC’s long-term view and strategy for India.

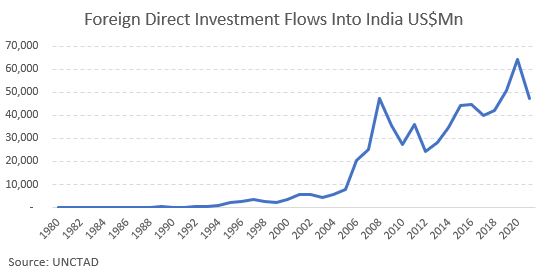

India has been an important destination for global institutional investors like GIC, given its long-term growth potential, and easing of foreign investment rules. Foreign direct investment (FDI) flows (see first chart below) and the role of private investment have risen as more sectors opened up and restructuring efforts continued, even during the Covid-19 pandemic. The domestic stock market has performed strongly over the last 25 years with INR returns of 13.5% CAGR (compound annual growth rate) and US$ returns of 10.1% CAGR.

Due to Covid-19, India like most countries, saw its economy contract with a GDP growth of -6.6% in FY2020-21, its worst recession since gaining independence in 1947, as lockdowns severely curtailed business activity. Despite initial setbacks, India was able to re-orientate quickly, with 60% of its 1.4 billion population fully vaccinated by the end of March 2022 (vs 4% at the end of June 2021 reflecting an increase of ~770 million in vaccinated people). As businesses adapted and restrictions eased, growth has picked up with a strong recovery projected, notably over the next two years.

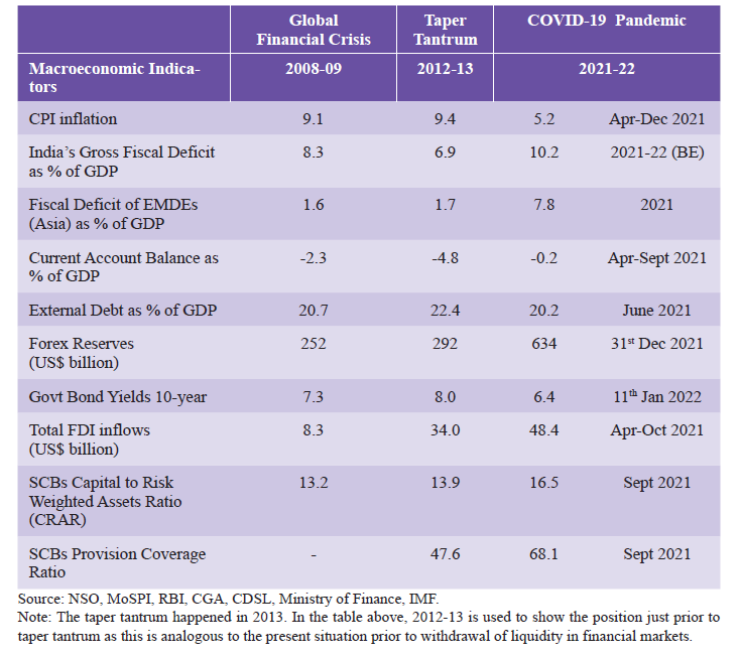

Comparison of macroeconomic indicators during the Global Financial Crisis, Taper Tantrum and Covid-19

India’s improved economic profile versus the Global Financial Crisis and Taper Tantrum in 2013/14

Labelled as one of the Fragile 5 during the 2013-14 Taper Tantrum when the INR depreciated by ~25% and bond yields spiked ~200bps, India’s macro imbalances have since narrowed due to fiscal and monetary prudence. Various vulnerability indicators (see second table above) such as current account deficit, forex reserves, external debt to GDP ratio, and asset quality of banks improved sharply as a result. This stronger economic profile is providing buffers against the recent tightening in global financial conditions and global commodity prices-led inflation. The well-coordinated policy responses, including the Reserve Bank of India (RBI)’s policy tightening and the Ministry of Finance (MOF)’s targeted fiscal support to cushion oil price shocks, should also help the economy to weather the current bout of negative terms-of-trade shock. India’s self-sufficiency in grain production would also help to limit much of the potential fallout associated with food supply shocks.

Longer term growth drivers

Pre-Covid, policy and reform measures such as the Goods and Services Tax, the Insolvency & Bankruptcy Code, and corporate tax rate cuts had already been implemented, whilst privatisation efforts continued during Covid-19. Also, given recent years of deleveraging, Indian corporates are in better financial shape to invest more with gross debt/equity ratio improving sharply from ~1x to 0.5x, and corporate profitability (as a % of GDP) rising to a 10-year high by FY21. Specific efforts that should help boost India’s capex and long-term potential growth include:

- National Monetisation Pipeline (NMP) launched in August 2021

The government plans to raise six lakh crore rupees (approx. US$77.2bn) over FY2022-25 by leasing assets to the private sector and investing the proceeds to create new infrastructure. The NMP covers a wide range of infrastructure (e.g. roads, ports, airports and railways; mining, power generation and transmission; and sports stadiums, warehouses and housing). This would help to co-finance, via public-private partnerships, the huge capex plan (well over US$1tn) of the National Infrastructure Pipeline over FY2019-25.

- Production Linked Incentive (PLI) scheme launched in March 2020

This scheme seeks to capture the trend of global manufacturing supply diversification through the “Make in India” initiative. The intention is to reap the potential of India’s young population, large economies of scale and scope to achieve higher productivity growth and competitiveness in exports, and reduce India’s import dependence. Manufacturing value added as a share of GDP in India is ~13%, far behind other emerging markets (EMs) in Asia (~20% or more in China, Indonesia, Malaysia and Thailand in 2020). The PLI scheme covers 14 sectors, which account for 40% of total imports. It is estimated to add a capex of four lakh crore rupees (approx. US$51.5bn) over the next five years, and generate an additional industrial capacity of 30 lakh crore rupees (approx. US$386.1bn) as well as over 3 million jobs.

- Digitalisation as a key source of growth and competitiveness

India has been able to rapidly advance digital adoption via widespread internet access through mobile devices. Teledensity improved from less than 1% in the early 2000s to 86% by December 2021, of which 98% was wireless. India’s cost per GB of data consumed is also one of the lowest globally at 50 rupees (approx. US$0.64) per GB, while the quantum of mobile data consumed per user is one of the highest at 14GB per person.

The government has consciously stepped up its efforts to digitise the economy. For example, the Unified Payments interface, developed by the RBI and leading Indian banks, facilitates digital interbank transactions. Aadhaar, India’s biometrics-based digital ID programme, is the largest in the world and enables accountability in online transactions. Since the launch of the Startup India Initiative in 2016, the number of new startups has risen to over 14,000 in FY2021-22 from only 733 in FY2016-17. India ranks third globally after the US and China in terms of number of unicorns. The number of active, India-based unicorns rose from nine in 2017 to around 90 by the end of March 2022, increasing the potential for further IPO activity down the line.

- Attractive growth potential in India’s public debt markets

India’s improving macro stability could potentially lead to its global bond index inclusion. India is the only major EM country that is not in any global bond index, and its bonds are under-owned by foreign investors relative to other EMs (1.9% vs 10.6% in China and 22.6% in Indonesia). If included, according to market estimates, benchmark-related active inflows of US$7bn per year could reach 10% foreign ownership by 2030. This could help provide financing for capex and reduce borrowing costs via lower bond yields. However, policy hesitancy may have delayed the inclusion beyond 2023.

- India’s sustainability agenda

We are encouraged by India’s pledge at COP26 to be net zero by 2070, and its other carbon intensity reduction and clean energy targets in the intermittent years. The launch of the National Hydrogen Mission in 2021 to accelerate plans to generate carbon-free fuel from renewables by 2047 so as to achieve self-reliance in energy, is another important milestone for India.

India’s population growth, urbanisation and industrialisation point towards greater demand for infrastructure investment, which has tremendous potential for supporting the sustainability agenda. India already ranks highly in terms of overall renewable energy production and attractiveness, and it will make its first issuance of sovereign green bonds in FY23 as part of its overall market borrowing to tap private capital for green infrastructure.

In 2021, GIC joined Bloomberg’s Climate Finance Leadership Initiative (CFLI) in India, and will continue to support and invest in India’s sustainability and clean energy transition.

GIC’s strategy for India

GIC had an early start in India given our proximity and confidence in the growth potential of EMs in Asia. Having invested in India’s public markets since the mid-1990s, followed by private equity, and subsequently, real estate and infrastructure since the mid-2000s, GIC ranks amongst the earliest and largest institutional investors in India.

As the size of our India portfolio and networks grew, GIC set up its Mumbai office in 2010. Our India Business Group (IBG) helps coordinate GIC’s investment approach across different asset classes and recommends an appropriate overall portfolio and partnership strategy for India. GIC has made investments in India in several sectors including financial services, IT services, real estate, infrastructure, healthcare and consumer goods. GIC also has a special focus on investments in technology-driven businesses.

Long-term partnerships on the ground are vital to GIC’s investment approach. Our partners provide access to opportunities, strong market knowledge, as well as investment and operational capabilities, which are especially important when investing in the private markets. In return, we provide long-term, flexible capital, access to our global network, professional and speedy execution, and fair terms. As a global long-term investor, we look to build assets and grow businesses that contribute to the growth and prosperity of the markets that we invest in. In India, we have been privileged to form many good partnerships with leading business groups, entrepreneurs and other stakeholders over the years.