A growing global economic and financial footprint

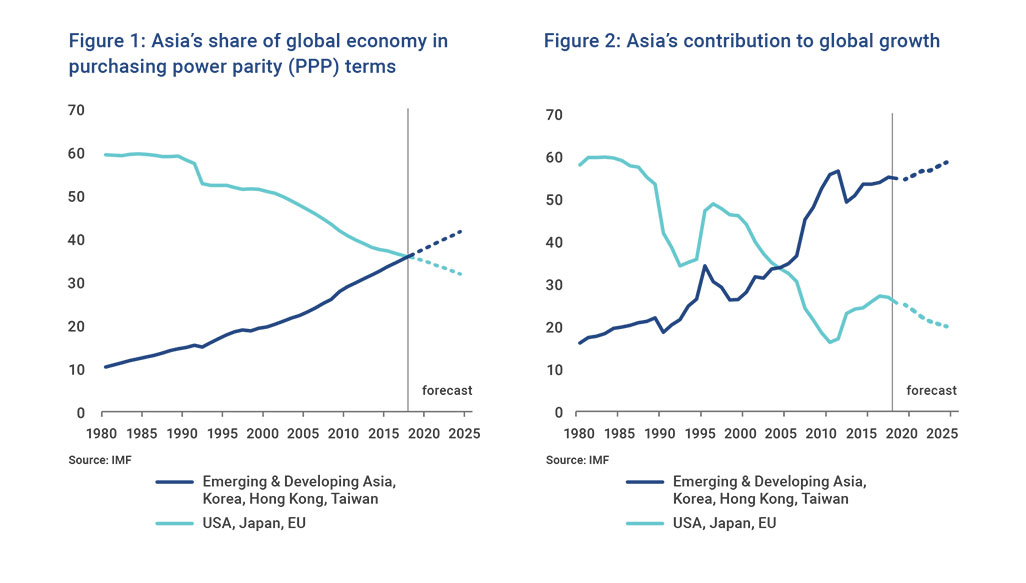

Asia’s economic footprint, in particular Emerging Asia’s, has been growing significantly. Excluding Japan, the region’s share of global Gross Domestic Product (GDP) rose from around 10% in 1980 to 36% today (Figure 1). Asia already hosts some of the world’s largest economies, notably China, now the largest economy and financial market after the United States. Asia’s growth rate is also outstripping that of other regions, accounting for approximately half of global growth last year (Figure 2).

At the same time, the nature of growth in the region has also been changing. While exports to the rest of the world remain a key driver, Asian economies increasingly rely on domestic and regional sources of growth due to increased supply-chain, trade, and financial market integration.

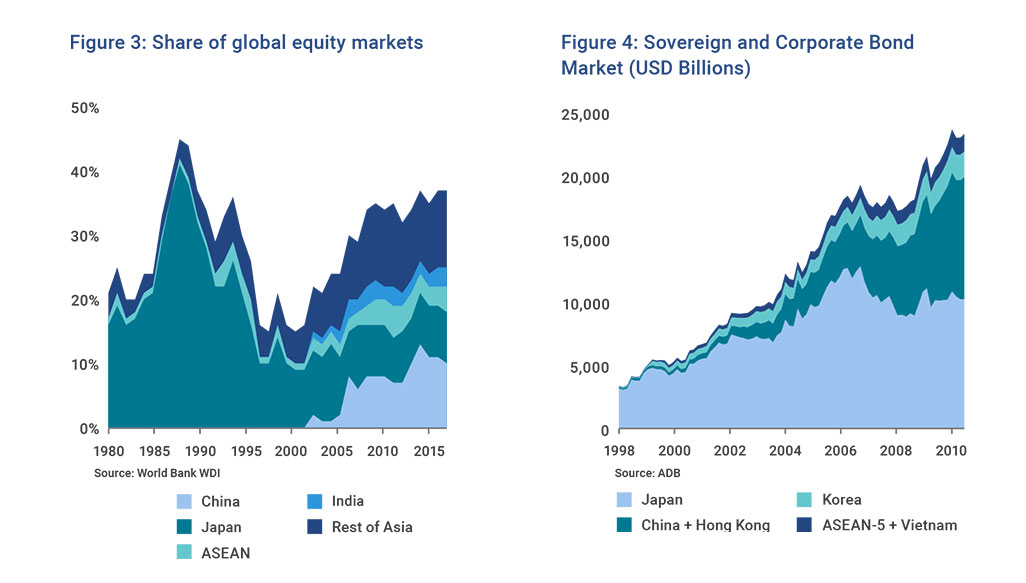

Change has also been taking place in Asia’s financial markets. In response to the rapid rise of Asian economies, its equity, bond and foreign exchange markets have grown, notably in Emerging Asia. The region’s equity markets command close to 40% of global market capitalisation today (Figure 3). The development of local currency bond markets (Figure 4) in the region has not only increased the scope of investible assets in the region, but also fostered stability by reducing the currency mismatch that was a problem for many Asian economies in the past.

Will Asia’s rise continue?

Asia is made up of economies at very different stages of development: very advanced economies like Japan, large emerging economies such as China and India, and other emerging economies which still have huge catch-up potential.

Despite the heterogeneity, three broad factors have driven Asia’s growth, which we believe will persist – its attitudes to globalisation and openness, improvement in its institutions, and the dynamism of its people:

- Asia’s growth path has been characterised by continual lowering of trade and investment barriers. With opening up, many countries have benefitted from technological catch-up.

- Asia has also had progressive reforms in its institutions. This is reflected in the improved business environment rankings for many countries in the region. For instance, the World Bank’s 2019 “Ease of Doing Business” report ranked 5 Asian economies in the top 15 (out of 190), with big economies like China and India climbing 50 spots or more over the last 5 years.

- The region’s people and businesses are driven and adaptable to change. Educational attainment has improved markedly. Some Asian countries also enjoy a demographic dividend.

While the region’s future growth may be slower as economies mature and populations age, it will still in aggregate likely outpace that of developed and emerging economies outside of Asia.

We believe three themes will underpin Asia’s potential.

First, there continues to be room for urbanisation and middle class growth in the emerging economies. The share of Emerging Asia’s population living in urban areas has risen to about 50%, which is still well below that of high-income countries at over 80% . The middle class has also grown rapidly in Asia, and is predicted to more than double over the next 10 to 15 years, driven by countries such as China, India, Indonesia, and the Philippines.

A second driver is continued investments in infrastructure and human capital. While the region has made much progress on this front, there is room to do more in Emerging Asia, where the infrastructure investment gap is estimated at about US$3.9 trillion or 10% of projected GDP for the 15-year period to 2030 . China’s Belt and Road Initiative (BRI) stands out with estimates of over US$1 trillion worth of infrastructure spending projected up to 2027. If successful, it can provide a big lift to the region, which needs significant infrastructure development and financing.

Likewise, investment in education will continue. For example, in Emerging Asia, enrolment rates in tertiary education are often still low with significant potential to grow, particularly in skills-based and vocational education. In advanced Asia, the continued upgrading of skills, expertise and innovation will support productivity growth. Asia is also attracting talent from all over the world.

A third driver of growth is deeper regional integration. While this will benefit Emerging Asia, it is also important for the more advanced Asian economies. Financial integration within Asia has notably increased, but is still lower than trade integration. About 60% of Asia’s exports and imports go to, or originate from, the region, but only 20% to 30% of cross-border portfolio investment and bank claims are intra-regional, leaving plenty of capacity for growth in cross-country investment flows . Another driver will be the continued opening up of Asia’s capital markets to foreign investors. For example, China A-shares has been increasingly added to MSCI’s emerging market benchmark index since July 2018. Although globalisation may progress more slowly going forward, together with regional integration, it is expected to support Asia’s growth story over the longer term.

Asia has challenges to overcome before it can deliver its full potential

Asia’s path going forward is not going to be smooth. There will undoubtedly be challenges that have to be overcome along the way.

One challenge is structural reforms, which must continue. Further liberalising trade and market access are critical to improving productivity and unlocking Asia’s growth potential. In advanced Asian countries, reforms will be key to raising the effectiveness of innovation and spur service sector expansion. Emerging Asia will need to address infrastructure bottlenecks, improve flexibility of the formal labour market, and raise access to healthcare, education, and financial services. The private sector could be encouraged to play a bigger role in several countries.

Asia is also vulnerable to geopolitical tensions. While most attention has been focused on North Korea, other flashpoints include the territorial challenges in the South China Sea. These are tail-risks that could disrupt Asia’s growth story and security situation.

One manifestation of these tensions is the growing trade and business restrictions between the US and China. This will affect not only China itself, but also the rest of Asia, due to the high trade dependency and regional supply chain integration. While some economies may benefit from trade diversion and the reconfiguration of supply chains, such tensions are harmful to the region overall. If the US and China impose 25% tariffs on all traded goods, the peak GDP loss in the near term will be sizeable for Asia as a whole, aggravated by negative sentiments and tighter financial conditions . The tensions are already causing a slowdown in regional trade. Many countries will be significantly worse off, losing the benefits from globalised markets and supply chains, and the sharing of knowledge, innovation, and technology that enable countries to progress together. In such a scenario, China and the other Asian countries will still be able to develop and upgrade their domestic economies. It is not likely that China’s growth and development can be stopped. But the fragmentation of markets and a drive for self-sufficiency will lead to slower productivity growth and misallocation of resources.

New technologies can help boost productivity and compensate for a shrinking labour force in some countries. However, they will also disrupt businesses and the job markets. Labour in more advanced economies remain exposed to the automation of routine tasks, due to higher wages and declining costs of capital goods. In Emerging Asia, automation threatens the traditional “development route” of labour-intensive manufacturing. This will require proactive policies to enable businesses and workers to adapt to and take advantage of new opportunities.

Lastly, Asia needs to overcome labour, natural resource, and environmental constraints. Some countries like China, Japan, and Thailand are aging and their labour forces are shrinking. In addition, there is a need for proper regulation, incentives and investment in green technology to address the resource scarcity and environmental challenges. This will have a big impact on the economies’ potential growth and their people’s well-being in the long run.

If Asia overcomes these challenges – and we believe the governments, businesses, and people have the resolve and capabilities to do so – the region will remain economically vibrant and attractive for investors. This will cement the global economic and financial shift to Asia over the long term.

How does GIC invest in Asia?

High economic growth does not automatically mean higher investment returns. At GIC, we target companies and sectors that benefit from current or future drivers of the economy, and invest via both the public or private markets across the region. As a long-term value investor, we look to buy the “growth story” before it is fully priced into valuations and stand ready to take advantage of potential market dislocations.

GIC has been an early and significant investor in Asia. Starting in Japan in the 1980s, and expanding to Emerging Asia from the 1990s, GIC focused on growing the Asia portfolio given our belief that the region will benefit from sustained structural improvements and outperform in the long term. One way GIC gained exposure to Asia was indirectly through multi-nationals. In the earlier years, these were good vehicles to use, because of their better governance and liquidity. However, with the rising number of strong, unique businesses established by domestic Asian firms, increasingly we have felt the need to gain direct exposures. Today, about 30% of our portfolio is in Asia, more than most global institutional investors. Even in the private markets, GIC ranks as a significant foreign institutional investor in the region.

Conclusion

Asia presents attractive opportunities across consumption-based goods and services sectors, including financial services, healthcare, education, and technology. Its global value proposition will increase further, fuelled by the continued rise of its middle class, infrastructure investments, and regional integration, backed by steady technological progress. While Asia has challenges to overcome, GIC is confident that these can be addressed, in particular through sustained structural reforms. As an early and steady investor in the region, we have learned valuable lessons and will continue to strengthen our capabilities and partnerships. This will help us play a positive role in Asia’s growth over the long term.